The business situation has slightly improved in September but remains dire.

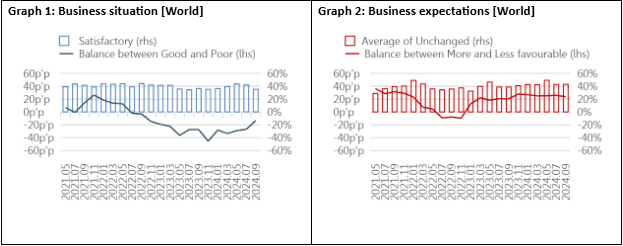

According to the September edition of the ITMF Global Textile Industry Survey (GTIS), business conditions have improved and are at their strongest point since September 2022. Recovery in South America and Africa has played a major role in this improvement. Nevertheless, no appreciable progress was seen in other areas. firm expectations are still high, with optimism staying steady at +25pp since November 2023, even though the state of the firm as a whole has not yet improved. Although order intake is still negative, it has been gradually increasing over the past ten months, especially in South America and Africa.

Graph 1: Business situation [World] Graph 2: Business expectations [World]

Source: 8th-27th ITMF Global Textile Industry Survey (27th: 15-30.07.2024)

With an average global backlog of 2.2 months in September 2024, up from 1.9 months in March 2024, order backlogs indicate a small upward trend. After increasing since July and rebounding from a low of 68% in November 2023, capacity utilization hit 75% in September. 66% of poll respondents in September 2024 expressed concern about weak demand, which has been the main issue since 2022. But with 63% reporting no cancellations, order cancellations have reached a historic low, particularly in South America.

Along the textile value chain, inventory levels are still normal; in September, 55% of businesses reported typical levels. Retail and wholesale clothing stocks in the USA have been increasing, which may indicate that the bottom has been reached.