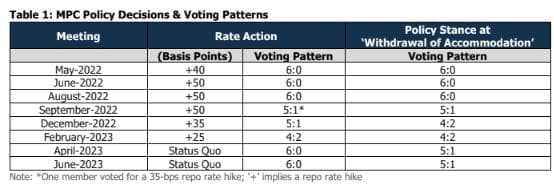

The Monetary Policy Committee (MPC) of the RBI maintained a status quo on the repo rate keeping it unchanged at 6.5% in its second bi-monthly policy meeting of the current fiscal. This marks the second consecutive meeting wherein the MPC decided to keep the repo rate unchanged after having raised it by a cumulative 250 basis points

(bps) during the last fiscal. The Liquidity Adjustment Facility (LAF) corridor was maintained at 50 bps with the Standing Deposit Facility (SDF) and Marginal Standing Facility (MSF) unchanged at 6.25% and 6.75%, respectively. The MPC maintained the policy stance at ‘withdrawal of accommodation’ reflective of RBI’s vigilance on the inflation

front. In terms of the view of MPC members, while the decision to keep the repo rate unchanged was unanimous,

the members were split over maintaining the policy stance at ‘withdrawal of accommodation’ with a vote of 5:1.

The decision to continue holding the pause button on policy rates comes at a juncture when retail inflation is seen moderating and domestic growth has been holding up well. Several high-frequency economic indicators such as GST collections, e-way bill generation, air passenger traffic, manufacturing and services PMIs continue to point towards sustained momentum in the economy. Though the RBI decided to keep the policy rates steady drawing comfort from the softening retail inflation, the central bank’s commentary reflects a cautious undertone. With inflation yet to see a durable easing to the medium-term target of 4%, the RBI reiterated its commitment to ensuring price stability. Risks to domestic inflation persist on account of a volatile global scenario, the uncertain trajectory of global commodity prices and domestic weather-related risks. Thus, a fairly resilient growth scenario coupled with inflation ruling above the medium-term target supports the possibility of an extended pause in the policy rates in 2023.

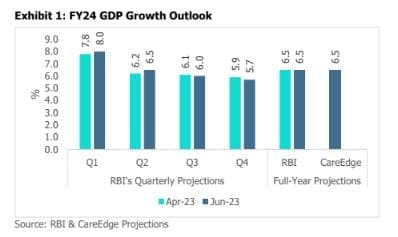

RBI Retains FY24 GDP Growth Projection at 6.5%

The domestic economic growth surprised on the upside, with GDP growth print at 6.1% in Q4 FY23. The economy’s better-than-expected performance in the final quarter took the full-year growth to 7.2%, higher than the advance estimate of 7% growth. The services sector continued to steer growth supported by a rebound in discretionary

spending as seen in the recovery of contact-intensive sectors such as trade, hotel, and transportation. More importantly, industrial growth picked up on the back of a rebound in the manufacturing sector and the healthy

performance of the construction sector. The manufacturing sector’s improvement comes as a relief given that it has been reeling under the impact of weak external demand and uneven domestic demand recovery. A healthy performance of the agricultural sector despite the impact of weather-related disruptions also supported the

domestic growth scenario in FY23.

The RBI retained its projection for real GDP growth at 6.5% in FY24 with minor shuffling in the quarterly growth projections. The RBI revised its growth forecasts slightly higher in the first two quarters of FY24 drawing comfort from the resilience in the domestic economy. With the domestic growth holding up well, we have raised our GDP growth projection to 6.5% for FY24 (from the previous projection of 6.1%). The easing in rural inflation, improving wages and robust agricultural output is likely to bode well for the fragile rural demand. However, weather-related uncertainties associated with El Nino could dampen the rural demand recovery. Although the recovery of the manufacturing sector in the last quarter of FY23 is encouraging, challenges from external demand slowdown are expected to persist. However, the lower drag from net exports amid moderation in the trade deficit would be supportive of growth. Overall, risks emanating from global vulnerabilities pose downside risks to the domestic growth scenario.

RBI Lowers FY24 Inflation Projection to 5.1%

Inflationary pressures in the economy have witnessed some cooling in recent months. Retail inflation eased to 4.7% in April 2023, the lowest level in the past eighteen months. This moderation was aided by a favourable base and lower food inflation. Despite the easing in food inflation, the elevated price pressures in select items such as cereals and milk remain concerning given their impact on household inflationary expectations. Core inflation after remaining sticky near the 6%-mark eased to 5.5% in April, the lowest level in nearly two years. However, services-

driven inflation stayed elevated as seen in the health, education and personal care segments.

The RBI revised its FY24 inflation projection slightly lower to 5.1% from its earlier forecast of 5.2%, bringing it in

line with our full-year projection. The RBI lowered its inflation projections for the first two-quarters of FY24 citing

moderating risks to inflation in the near term. However, the central bank emphasized the need for vigilance amid

risks from price pressures during the latter half of the year. Developments related to the monsoon and risks from

global commodity prices remain the key monitorable. 7.8 6.2 6.1 5.9

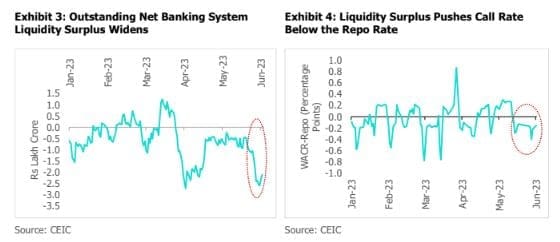

Liquidity Surplus in the Banking System Widens

The average daily outstanding (net) liquidity in the banking system which was already in surplus widened further

close to Rs 2 lakh crore in June so far. This increase in the banking system liquidity has been driven by the increase

in government spending, decline in the currency in circulation and redemption of government bonds. The decision

to withdraw Rs 2,000 currency notes from circulation further boosted short-term liquidity in the banking system.

The higher liquidity surplus in the banking system pushed the weighted average call money rate below the repo

rate since May-end. In line with the RBI’s policy stance of ‘withdrawal of accommodation, the RBI has been

conducting variable rate reverse repo auctions in order to drain out the build-up of liquidity from the banking

system. Going ahead, the RBI is expected to continue the variable reverse repo auctions to manage liquidity

conditions for efficient transmission of the monetary policy. Moreover, the liquidity surplus could witness some

moderation in June owing to the advance tax outflows and GST payments.

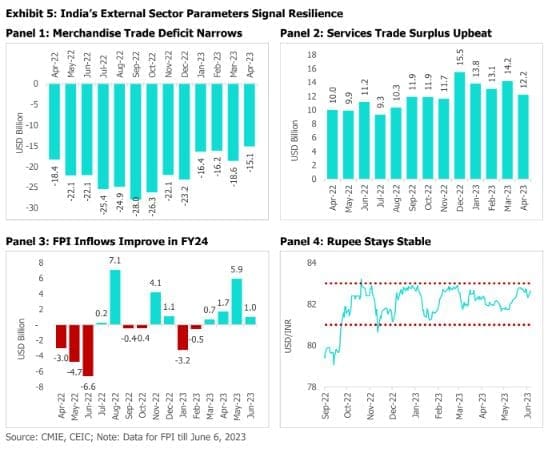

External Sector Scenario Improves

India’s external sector scenario has continued on the improvement path since the last MPC meeting in April. India’s

merchandise trade balance has witnessed a notable moderation in recent months after staying at elevated levels for most of FY23. This decline in the trade balance was aided by lower commodity prices and moderation in imports.

India’s current account deficit (CAD) is expected to moderate in the final quarter of FY23 gaining support from healthy services exports, remittances and easing pressure on the merchandise trade balance. We estimate CAD to

be at 2.1% of GDP in FY23 with a projected improvement to 1.6% in FY24. On the investment front, there have

been foreign portfolio investments (FPI) inflows worth USD 8.6 billion so far in FY24 as against outflows of USD

5.5 billion in FY23. Going ahead, a stable rupee, positive real rates and favourable growth prospects bode well for

the sustenance of this trend. Improvement in foreign fund inflows and improving prospects for the current account

deficit are likely to be supportive of the rupee which has remained largely stable so far in 2023.

Way Forward

While the RBI decided to keep the policy rates unchanged for the second consecutive meeting, it has continued to

emphasize on bringing the retail inflation closer to the target of 4%. Amid a volatile global economic scenario and

lingering risks to domestic inflation, it is prudent that the RBI has followed a wait-and-watch strategy. With concerns on the growth front abating and CPI inflation likely to remain above the 4% target, we expect a status quo on the policy rates in 2023.