Overview of Asian Textile Industry & Competitor Analysis

Asian Textile Industry

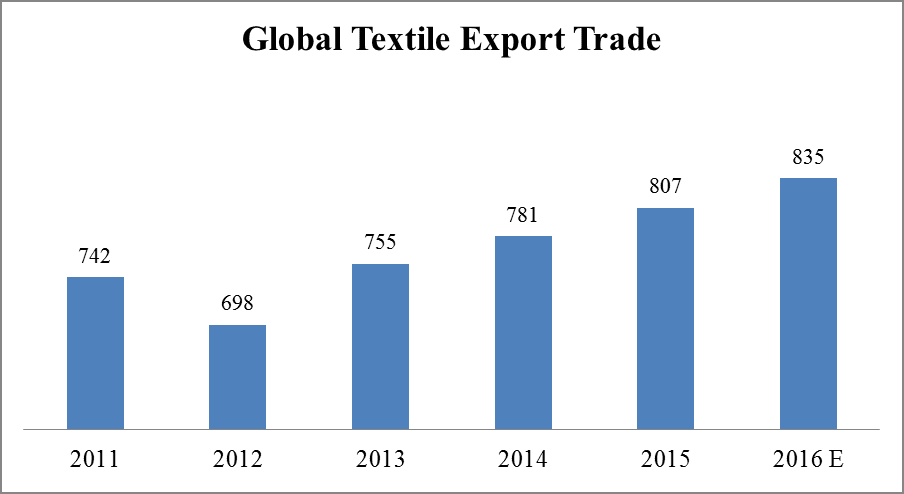

The global textile& apparel trade is increasing at a CAGR of 3% since last few years. Asia is the main hub for textile industry. China is the major exporter with total share of 37% in the global trade of textile & apparel sector followed by other countries like India, Bangladesh, Indonesia, Vietnam & Cambodia. The textile industry is highly labor intensive industry. Hence, lower cost of production & cheap labor are the main reasons for growth of Textile industry in the Asian countries. USA, European Countries, UK & Japan are the major export market for Asian countries. China controls about 40 percent of global textile markets & India claims second position.

China

China has dominated the textile and garment industry for the past 30 years, and remains the single largest producer and exporter of textiles and clothing, thanks to its low production costs. It has well-established supply chains, as well as good infrastructure and expertise in textile and apparel products in much larger volumes. No single emerging country in South East Asia can yet hope to match China in all of these capabilities. Hence China will likely remain the leading textile and apparel sourcing country in the region over coming few years. With labour, land and regulatory costs on the rise, analysts predict that the industry is about to undergo a shift to South East Asia and beyond. Despite competition from cheaper South East Asian nations, China will remain the dominant player in the industry for some time to come — given the size of the domestic market, supply chain concentration and the scale benefits it has accumulated over the years. These things are hard to replicate. Emerging countries in South East Asia are increasingly challenging China’s dominance. Many international firms are adopting the “China plus one” strategy, whereby they retain a production base in China, yet open another facility in a low-cost Asian country. It’s a sound diversification strategy to reduce risk, most suited to larger businesses that can afford to scale up.

India

India is highest growing economy today on world’s map. With abundant raw material availability & stable government, strong industrial growth is forecasted in near future. Textile is one the most ancient industries. Today, textile sector is one of the largest contributors to India’s exports with approximately 11 per cent of total exports. The industry realised export earnings worth US$ 41.4 billion in 2014-15, a growth of 5.4 per cent, as per The Cotton Textiles Export Promotion Council (Texprocil). The Indian Textile Industry contributes approximately 5 per cent to India’s Gross Domestic Product (GDP), and 14 per cent to overall Index of Industrial Production (IIP). The Indian textiles industry, currently estimated at around US$ 108 billion, is expected to reach US$ 223 billion by 2021. The industry is the second largest employer after agriculture, providing employment to over 45 million people directly and 60 million people indirectly. The Indian textiles industry is extremely varied, with the hand-spun and handwoven textiles sectors at one end of the spectrum, while the capital intensive sophisticated mills sector at the other end of the spectrum. The decentralised power looms/ hosiery and knitting sector form the largest component of the textiles sector. The close linkage of the textile industry to agriculture (for raw materials such as cotton) and the ancient culture and traditions of the country in terms of textiles make the Indian textiles sector unique in comparison to the industries of other countries. The Indian textile industry has the capacity to produce a wide variety of products suitable to different market segments, both within India and across the world. The future for the Indian textile industry looks promising, buoyed by both strong domestic consumption as well as export demand. With consumerism and disposable income on the rise, the retail sector has experienced a rapid growth in the past decade with the entry of several international players like Marks & Spencer, Guess and Next into the Indian market. The organised apparel segment is expected to grow at a Compound Annual Growth Rate (CAGR) of more than 13 per cent over a 10-year period.

Bangladesh

While the rest of is Asia disappointed in terms of export revenue in 2015, there was one surprising anomaly to the pattern – Bangladesh. Bangladeshi export earnings rose to $31.5bn in 2015, thereby setting a new record for the South Asian country. This phenomenal success can be attributed to Bangladesh’s growing apparel industry, which accounted for over 83 percent of total exports.

As global demand for cheap clothing rises rapidly, Bangladesh’s position as the second biggest exporter of garments in the world continues to hold strong, which is mainly due to its large population and low labour costs. In fact, according to the World Bank, the country’s GDP is expected to grow to 6.7 percent this year, which will make Bangladesh one of the fastest growing economies in the world.

The textile and apparel industries provide the single source of economic growth in Bangladesh’s rapidly developing economy. Exports of textiles and apparels are the principal source of foreign exchange earnings. By 2013, about 4 million people, mostly women, worked in Bangladesh’s $19 billion-a-year industry, export-oriented ready-made garment (RMG) industry. Bangladesh is second only to China, the world’s second-largest apparel exporter of western brands. Sixty percent of the export contracts of western brands are with European buyers and about forty percent with American buyers. Only 5% of textile factories are owned by foreign investors, with most of the production being controlled by local investors. The Ready-Made Garments (RMG) industry occupies a unique position in the Bangladesh economy. It is the largest exporting industry in Bangladesh, which experienced phenomenal growth during the last 20 years. By taking advantage of an insulated market under the provision of Multi Fibre Agreement (MFA) of GATT, it attained a high profile in terms of foreign exchange earnings, exports, industrialization and contribution to GDP within a short span of time.

Indonesia

Robust economic growth and rising purchasing power make Indonesia – the world’s fourth most populated country – an attractive market for textiles and clothing. Both local and foreign companies are vying for market share. Rising costs are giving domestic producers a hard time as they try to fend off overseas competition, but technological modernization, improving labour skills, better infrastructure and not least the relatively low rupiah alter the picture in their favour. Local textile producers depend almost entirely on imported cotton, since domestic farmers are unable to satisfy even 1% of national demand. This makes yarn spinners vulnerable to the fluctuating global prices and has forced a number of small businesses to close up shops, though larger ones are in a stronger position, thanks to their greater stockpiling ability and better access to capital. The principle buyers of yarn from Indonesia are China and Japan, while textiles and textile products go mostly to the US, the EU and Japan.

Vietnam

Vietnam has a lower cost base than China and India, although higher than Bangladesh and Pakistan. The textiles and apparel industry is actively supported by the government, and relatively significant currency depreciation makes the country’s exports competitive. The local workforce is still largely of a low-end skill base, however, meaning that Vietnam’s best sourcing opportunities are still in basic designs and standard types such as woven garments and baby wear products. The total export turnover of the garment sector reached $24 billion in 2014 and $27.5 billion in 2015, and it is expected to reach $31 billion by late 2016. Plentiful competitively priced labor giving the country a distinct cost advantage; and supportive government policies, including incentives to attract foreign direct investment.

Cambodia:

The garment and textiles industry has thrived for about two decades now. Growth skyrocketed when the normalized trade relationship went into effect with the United States and the European Union in 1996 and 1997. From humble beginnings with exports worth US$27 million in 1995, the sector grew 200-fold and by 2014 provided more than half a million jobs for young Cambodians. . The garment sector accounted for some 8.5 per cent of all employment in the country. Exports of the garment sector grew by a still substantial 8.3 per cent to $5.4 billion. The continued growth of garment exports is driven mainly by strong demand from European buyers

Source: UN Comtrade & Suvin Analysis

Total Export in 2015 = 50 Bn. USD

Total Export in 2015 = 105 Bn. USD

Total Export in 2015 = 336 Bn. USD

Source: UN Comtrade & Suvin Analysis

Summary

This very brief outline illustrates that China still holds the unique position in textile and apparel manufacturing however, it certainly is no longer the cheapest option available. It is still the dominant player, and will likely still account for the largest share of global textile and apparel sector, but other countries in South and South East Asia are now considered for certain product segments, and China’s position will be further assailed in the years to come by these emerging Asian countries. India is the most powerful competitor to China’s textile industry. It owns a huge and highly competitive textile industry and has become the world’s second largest cotton textile supplier. Today, Indian economy is in transition phase. Our Prime Minister Mr. Narendra Modi is taking good initiatives to attract foreign investments from Japan, China, USA and other developed countries. Many other foreign nations are eyeing on Indian economy for investments. Our Vision for textile & apparel sector should bring the right environment for investors by creating good infrastructure, skill development, Government policies & marketing platforms.

Let us carve out…

Better tomorrow!!!