SOS – YARN SPINNING COMPANIES IN DISTRESS

– Sanjay K Jain, President NITMA

In my business life, I have not seen a worse situation than this, where such a big disparity is there between spot cotton prices and yarn prices. This disparity for such an extended period of time shows there is a deep rooted problem and it’s not a temporary feature. The current isolated spurt in Indian cotton prices has aggravated the situation to an extent that many can hear the death knell. The more disturbing fact is that no domestic yarn buyer is hassled or is rushing to buy yarn — they know cotton prices have moved 50% and yarn just 20% — still no anxiety !!! International buyers have diverted their orders as cotton in India has increased much much more in comparison to international cotton prices.

Indian spinners have been going through a very difficult time over the last 2 years despite cotton prices being reasonably low due to a demand supply imbalance created out of new spinning mills coming up in some States (viable due to incentives rather than fundamentals) and slow demand locally due to two successive poor monsoons and overall subdued sentiments in the globe. Exports have failed to cheer us up due to the disadvantage created by FTAs of our competitors with the big buying nations and we as usual not able to break any ice anywhere.

Cotton yarn has suffered further as the Government felt that yarn needs no incentives. It’s true that yarn needs no more any investment incentives but it surely needs incentives to export. Requests went unheeded by the Govt from various Associations because they didn’t go into the details of demand – supply minutely or tried to understand the plight of spinning industry (though its classified as a stress industry by the Banking sector). The recent RBI Financial Stability report stated that Textiles had the highest slippages from Standard Account to NPAs I.e. 8.8% in 2015 and the way the industry is going 2016 is going to be worse.

Indian spinning industry is the most developed segment of the textile and clothing industry. It is a market leader in the global markets and we have 30% exportable surplus, which is being exported, all across the world. Hence it seems to be an industry needing no assistance, as the Government (Central & State) has given it a lot of incentives over the years leading to the industry coming of age with the best technology. However surprisingly the excessive and long term continuation of incentives has been the bane of the industry. It has grown no doubt but more on incentives rather than fundamentals. The Central Govt realised this and as a first step curbed incentives to the industry and finally stopped all incentives. However State Governments (Gujarat Maharashtra, Andhra, Rajasthan, MP etc.) came in with even higher incentives leading to the industry continuing its expansion.

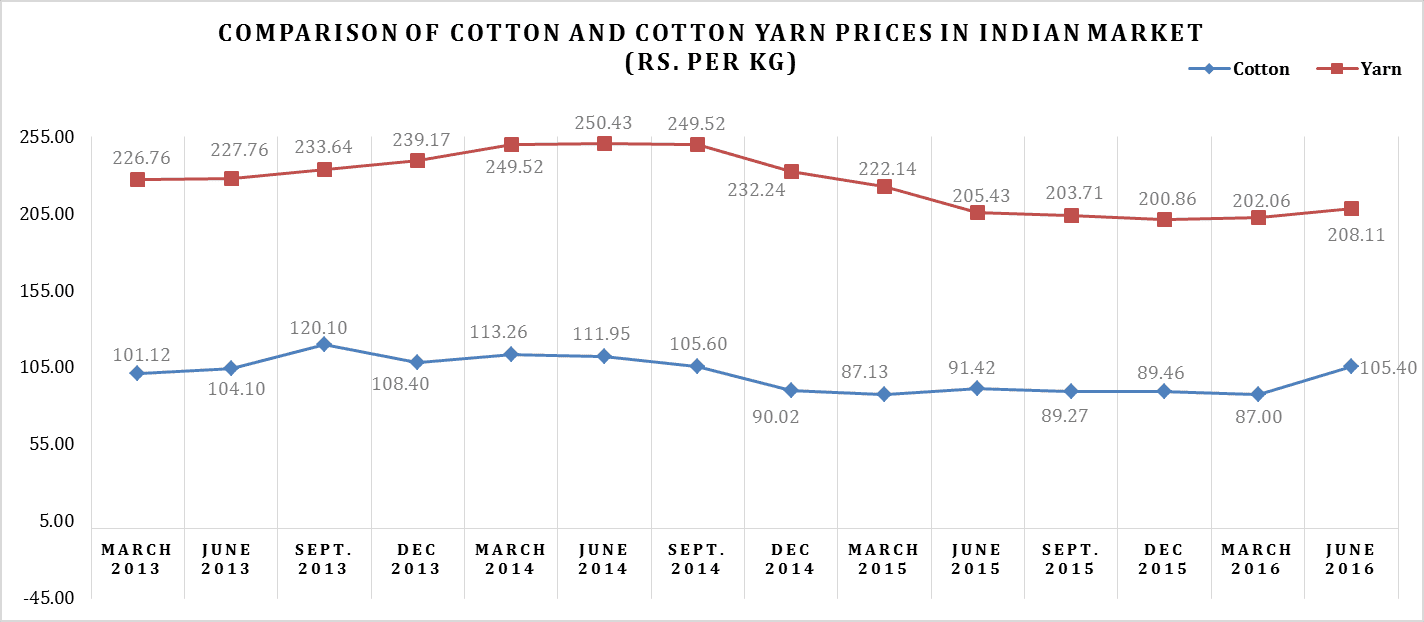

The state of the spinning industry can be further understood by the below chart which shows how the margin over cotton for the yarn industry has shrunk despite power, labour and other overhead costs going up. Margins instead of going up has come down and is today at a cash loss level.

As visible, cotton to yarn had a value addition of Rs 125/kg in March 2013 and went up to Rs. 144/kg in Sept 2014. Since last 1 year its been down to Rs. 115/kg and now its has come down to Rs 100/kg. Hence in last 3 years, contribution from yarn manufacturing has reduced by 25% while manufacturing costs have gone up by about 10% !!!

Source: Office of Textile Commissioner data base, July 2016 and Ministry of Textiles, July 2016

We live with hope that things will improve, however instead of seeing green shoots suddenly the industry faces a dark black tunnel through which many may not get through to see the light of the day.

It’s a serious crisis, hence kindly read me out (even if you disagree or find it boring)

Why are we here today ?

- Unplanned and illogical incentives being given for building spinning capacities (so much that it’s practically irresistible for one to not invest (Central Govt has finally understood, but State Governments still haven’t)

- Lack of any authentic crop and stock data in India despite being the largest producer and 2nd largest consumer.

- No clear cotton fibre policy hence no system of planning exports, stock to use ratio and other cotton developmental issues – working in an ad hoc fashion and leading to lobbying by different interested factions.

- Wrong and misleading cotton estimates from leading agencies /associations — gave a false notion that the country had enough cotton — agree its difficult to estimate, but if so then better not to give estimates

- Crop size in 2015-16 season is turning out to be substantially lower than estimated, catching spinners on the wrong foot. Quality cotton was exported at low prices and now cotton being imported at high prices (industry losing its main competitive advantage to competing nations).

- CCI acting like a trader when it comes to sell cotton – it surely helps farmers by picking up cotton but when disposing works simply as a trader without any vision of price stabilisation, industry service etc. This year small open bids were made by traders for CCI cotton raising the price level everyday which acted as a market indicator for price levels

- MCX/NCDEX is for hedging and price discovery, however its 99% run by traders and speculators (many who have nothing to do with cotton) and hence disrupts the physical market equilibrium. No action taken to rein steep rises in short times, allowing a free run to bulls. Curbing volatility of any nature is one of the prime roles of a regulator.

- The Government turning a blind eye to the spinning industry without understanding the facts

- TUF payments delayed and companies penalised for system errors by Banks in filing TUF claims

- Retrospective amendments made to deny benefits under Incremental Export Incentives – industry had to goto Court for justice

- Export incentives given to all segments of the industry excepting Yarn under MEIS and subvention — does the end user industry in India have the capacity to consume Indian yarn ?? India leads in exports not because we are the best, but because spinners have no choice but to undercut and sell yarn in exports to offload the excess spinning capacity

- The Rupee has weakened much less than most other currencies, even yuan has depreciated more over the last one year !!!

- Domestic consumption has remain muted due to 2 consecutive poor monsoons, fabric imports, and overall low sentiment in the economy

Today the way the spinning industry is placed, there seems no hope for the industry – we have excess capacity, which has to be dumped to China at below cost prices to keep the mills running. High fixed costs makes production cuts difficult. As a result NPAs are increasing, mills are partially or fully closing down on one hand while new investments are coming on the other hand. Old and new mills have a cost differential of 10% in an industry, which doesn’t even have a consistent Net Profit margin of 5%. Government is sitting peacefully and hoping as value added industry grows the balance will set in (don’t know how they expect industry to get through these prolonged times before value added industry catches up !!)

It’s amazing that despite this unprecedented and isolated increase of Indian cotton prices in 3 months, the Government has not come out in any visible fashion to understand the issues and problems. Weak and small mills have been left to the mercy of God to wither away with the strong bull winds as the world looks on. There hasn’t been even a statement from the Government !! Of course some mills that stocked cotton are making big gains out of this sudden boom in cotton, but the health of majority has got critical.

Anyway we live in hope and with a new Cabinet rank Minister we expect that the Government shall pay heed to the spinning industry problems and work with it to find solutions to atleast breakeven. We have everything that spinning industry needs, still we are suffering – a real pity. Indian Textile Industry is at a very important threshold and it’s now or never. China’s cost escalation has given India a golden opportunity to capture a bigger pie of the large global market and up its share from 4 to 5% to 10% over the next decade.

What we feel the Government can do (in order of priority):

- Allow immediately from April 1, 2016 MEIS and interest subvention for yarn industry

- Cotton fibre policy to ensure the country’s main competitive advantage i.e. cotton is leveraged fully and a healthy stock to use ratio of cotton is maintained. Our cotton to stock ratio (except 2015) has been always one of the lowest in the world ranging from 8 to 12% as against the world average of about 30 to 40%.

- Design a comprehensive, scientific and unbiased system for crop forecast and arrivals

- Create a balanced All India policy in consultation with States to ensures valuable Government money goes into developing the Textile Industry in a balanced manner (States giving incentives without seeing the National Picture is detrimental to the industry as a whole)

- Release data by DGFT of cotton and yarn exports/imports on real time basis

Conclusion:

Sincerely hope the step motherly treatment to the existing spinning capacity with high leverage and created out of incentives won’t be allowed to wither away. Spinning is a capital intensive industry and is very important for the value added industry to develop and thrive.

We should not forget that such isolated rises in domestic prices of raw material will make the whole value chain uncompetitive and the logic that we shall take the space occupied by China will go adrift. The Rs 6000 crore package given to garment industry is already more than nullified by this sudden spurt in domestic cotton prices and the future price index reflects that its not a temporary phenomenon.

Last but not the least, we should not forget that our biggest competitive advantage is our availability of cotton fibre. India cannot afford to fritter away its biggest competitive advantage – we have built our yarn economics on the same and need to take it forward to fabric and garments. Lets hope a comprehensive and well thought out long term policy/ strategy is put in place before its too late.