Shri S. Hari Shankar, Chairman,

Textile Machinery Manufacturers’ Association (India)

The Textile Engineering Industry (TEI) in India is one of the five key Engineering Sectors responsible for the growth of the Indian economy. It consists of more than 1400 units, with a total investment of approx. Rs.7,800crore. More than 80% of the units are SMEs. The total installed capacity is approx. Rs. 9100 crore. The industry provides direct/indirect employment to > 250,000 people. The TEI contributes greatly to the competitiveness of the Indian Textile Industry (TI). It meets 45-50% of the demand of the Indian textile industry.(Source: Textiles Committee Survey & TMMA)

Production

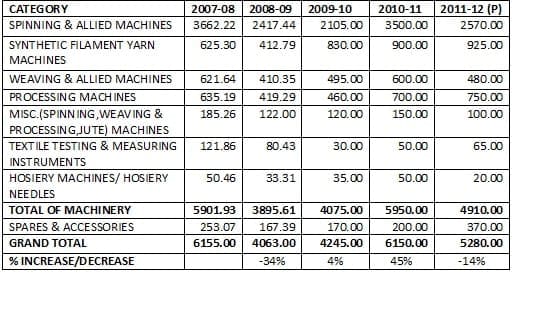

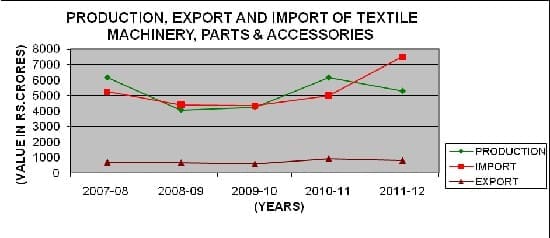

It is a matter of concern that the textile engineering industry was not able to grow steadily during the last 5 years. This may be seen from the table below:-

(Value in Rs.crores)

The unprecedented recession during 2008-09 & 2009-10 had shattered the pace of growth of the Indian Textile Engineering industry. The companies, which increased the capacity to meet the hyped demand from the domestic textile industry, suffered the most. Their equity took a severe beating in the market. The after-shocksof 2011-12 also rattled the industry and today it is living with the hope ofa positivegrowth during 2013-14 with sustained demand from the domestic textile industry.

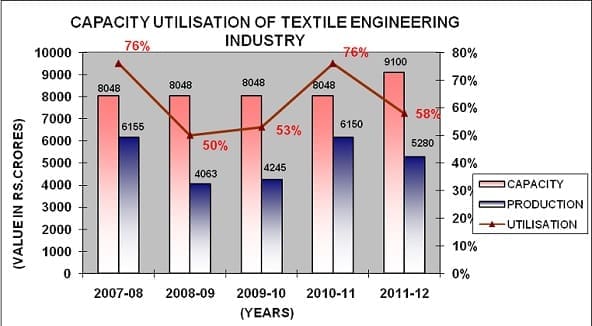

The capacity, production and utilization chart also shows how the domestic machinery manufacturers suffered during 2011-12.

The above chart shows how the textile industry became over dependent on imports steadily from 2009-10 onwards. While the domestic production has gone down due to less demand, imports have surged ahead. This is only due to the import of second hand machinery and also the cheaper imports from China. In all the categories, price factor ruled in favour of China which is becoming our main competitor. Chinese Companies’main advantage is that they are getting 11% subsidy from their own country, subsidy(duty exemption) in India and the TUFs benefits. They can afford to reduce the cost to a considerable extent. The Indian companies are paying several duties and taxes which are not included under CVD,thereby rendering the Indian companies uncompetitive to that extent.

Technology/Capacity:

- Ginning & Spinning:The entire range of Spinningmachinery manufactured in India, including ginning machinery, blow room machinery, cards, draw frame, combers, speed frame, ring frame, ancillary machinery, two for one twisting and auto-cone winding machines and parts and accessories,in general, are at par with international standards.

In ginning there are innovations to control the contamination in cotton by reducing human handling, maintaining humidity in pala houses and bins, auto feeding etc. There are 5/6 manufacturers in ginning.

- Capacity of ginning machinery is adequate and there are exports and practically no imports.

- There is adequate capacity in spinning. The total capacity of Ginning and Spinning is Rs. 4,561 crores. It meets over 75% of domestic requirement. In the coming years, it is likely to meet 90% of the requirement. There are domestic as well as foreign players.The technological gap is minimal.

- Auto Coner with auto feed and auto doff & high speed rotor spinning machines are not manufactured in the country

Weaving:The totalcapacity isRs. 703 crores.

- Weaving Preparatory:The technology is at par with international standards. There is enough capacity and production. Some of the reputed manufacturers are PrashantGamatex Pvt. Ltd., Ahmedabad, JupiterComtex Pvt.Ltd., Ahmedabad, etc.

- Weaving(Shuttle loom):Many manufacturers are supplying almost 40,000 to 50,000 powerlooms per annum. There are few manufacturers of automatic shuttle looms for which demand is less.

- Weaving (Shuttleless Looms): A number of manufacturersof old technology Rapier looms (Crank Beat-up) has come into existence. These numbers are on the rise. Present installed capacity is almost 16,500 per annum, though production has not reached beyond 2,000 per annum. However demand is increasing, it is hoped that within a span of another 2 years there would be approx. 25 manufacturers in the country. It is assumed that shortage of labour is responsible for increase in demand for this type of low cost low tech shuttleless looms.

- New technology rapier looms (Cam beat up) have been developed indigenously. But the same was not tested commercially. The preference for second hand looms and cheaper Chinese looms are responsible for nil demand. Things may change if the Government restricts the import of second hand looms. But as the things stands today, it appears to be a far cry.

- New technology Air Jet Loom has been developed indigenously. Though it has made its presence felt in some centres, the commercial success is still missing. The reason is very simple. Why one should buy the untested loom when the second hand loom is available at 50% cost of domestic loom?

- New technology water Jet Loom has also been developed. Its cost is ⅓ of the imported new loom. Here the question is how the domestic manufacturer would be in a position to offer same quality of imported loom at this cost. At the same time if they make it more sophisticated, the increase in cost will jeopardise the marketing because the second hand water Jet looms and Chinese new looms are cheaper. Therefore, the commercial success is still far off.

- Synthetic Machineries:The capacity is Rs. 1,000.00 crores approx. All kinds of synthetic machines such as Draw Texturising, TFO Twister, H.S. Winder etc. except fibre/filament manufacturing chemical plant,are produced. India is self sufficient in such machinery. There are also exports to different countries. We are competing with the reputed manufacturers of the world on equal footing. There is practically no import as there is no technology gap.

Most of the components of the synthetic fibre/filament mechanical processing machinery are made in India. Surat, Rajkot, Surendranagar are the main centers for the manufacture of spindles, spindle pots, spindle inserts, etc. Only critical electronic equipment like PLC controls, servo motors etc. are imported.There is no manufacturer of fibre/filament producing machinery except PP production line.

- Processing Machinery:The total capacity is approx. Rs. 900 crores.

There are more than 50 manufacturers of processing machinery in the country. Almost the entire range of processing machinery is now being manufactured in the country, with continuous scouring, bleaching, mercerising, washing, dyeing plants, preshrinking ranges and more, being produced by domestic manufacturers. The indigenous machinery available now competes on an even footing with their European counterparts with low material to liquor ratio, and is capable of processing fabric with comparable results at a very reasonable cost. All critical electronic components and equipments are imported. All other types of parts and accessories are also made in India.

For batch processes perhaps, we have the best quality machines when compared with other countries. Quality of textiles processing in Indian machines is at par with international standards. Technology gaps exist only in case of special purpose processing and finishing machinery and continuous plants. Now-a-days, this gap is also getting reduced.

Many hi- tech machinery are being manufactured in the country for e.g. Continuous Bleaching Plant, Dyeing Plant, Washing range, Preshrinking Range, Indigo dyeing Plant etc.

Existing capacity meets over 50% of the requirement

- Testing & Monitoring Equipments

The Indian textile engineering industry started developing testing and monitoring equipment in the 60s and today a wide range of high quality latest generation testing and monitoring equipment is being manufactured in the country. Almost 80% of the requirement is met by the domestic manufacturers. The total capacity is Rs.220.17 crores.

In this segment critical components and electronic controls are imported.

- JuteMachinery

Even in jute machinery the percentage share of demand is over 60%. There are half a dozen good manufacturers of jute machinery in the eastern sector. Many items of jute machinery are being manufactured in the country. The total capacity may not exceed Rs. 70 crores.

Lagan Engineering Co.Ltd., Kolkata is the major manufacturer of jute machinery and its parts, components and accessories. There are some small engineering units also manufacturing jute machinery parts and accessories in Kolkata, West Bengal.

- Parts/Components and Accessories:Capacity is almost Rs. 1,000 crores.

The parts/components and accessories also play a major role in manufacturing and maintenance of the textile machineries.These are:Bearings, Beams, Bobbins, Bobbin Holders, Bushes, Card Gauges, Ceramic Guides, Cone and Tubes, Cops-Aluminum/Steel, Drums, Filters, Flat Tops, Motors, Needles, Pins, Pirns, Belts, Rollers, Humidifiers, Over Head Traveling Cleaners, Shuttles,Healds, Reeds, Spindle Tapes, Trolleys, etc.

- Except some critical parts, most of the items are manufactured

- High speed cam dobby, electronic dobby and jacquard not manufactured

- Machinery items not manufactured

It is true that hi-tech garment making machinery and knitting machinery are not made in India. There is of course no shortage of ordinary domestic sewing machines and low tech knitting machines. The decentralized character of the hosiery and garment sector was not conducive for indigenous development.

The capacity of domestic hosiery and garment making machinery is approx. Rs.70 crores.

Similar is the case of nonwoven and technical textiles machinery. There was very little demand in the past. However, there are many technical textile items which are being manufactured in indigenous machines eg. Glass fiber fabrics, fish nets, mosquito nets, filter fabrics etc. etc.

The Indian Textile Engineering Industry had been playing a significant role in the growth and development of the textile industry in the country over the past 50 years. But it should have grown further to meet the entire demand of the domestic textile industry. It did not happen due to various reasons. China has outgrown our industry and has become the largest producer of textile machinery in the world. The comparison is given below:-

- Comparison Textile and Machinery Industry with China

Chinese textile industry has installedspindleage ofapprox. 120 million spindles, 7.20lacsshuttleless looms.Total textile production is approx. US$ 565 billion, with an export of approx. US$ 150 billion. Its textile machinery industry produced approx. Rs.500 billion worthof textile machinery. As a matter of fact China became the largest producer of textile and textile machinery in the world. Import of second hand machinery is highly restricted. Practically there is no such import. Chinaencouraged/forced global textile machinery players to set-up manufacturing base in China (through investor-friendly FDI/restriction to import if no local manufacturing set-up/ VAT acts as duty). Entire range of high tech machines is being produced.

As against the above, in India, the installed spindleage is approx. 42 million (approx. 34 million working spindles) and shuttleless looms about 1.20 lakh. Total textile production isapprox. US$ 62 billion while the export is approxUS$23 billion. The position is less than ⅓ of China in textiles.

Highest production of textile machinery was in 2007-08i.e. approx. Rs.63 billion which works out to 12-13% of China. Import of second hand machinery is freely permitted (including for modernization!). Only a part of high tech machines are in sectors other than spinning, the textile industry is considerably import-dependent.

- Future prospect

The Indian textile industry is very critical to the Indian economy. It contributes 4% to India’s GDP, 14% to India’s industrial production & 17% to India’s export earnings. Further, it is the 2nd largest employer after agriculture, with direct employment to over 35 million people. With ever growing population approx. @ 20 million per annum, the demand for fabric would grow. The rapid changes in fashion and style would facilitate development of niche category and improve the profitability of the textile industry.

India’s textile & apparel industry (domestic + exports) is expected to grow from the current Rs. 3, 27,000 crores (US$ 70 Bn) to Rs.10, 32,000 crores (US$ 220 Bn) by 2020. (Source: Technopak). The assessment, though an ambitious one, indicates the future of the textile engineering industry and its scope. We may not catch up with China, but may improve our position to a considerable extent.

A vibrant Indian textile industry calls for a strong Indian textile engineering industry (TEI) to provide a state-of-the art textile engineering solutions, to meet the growth potential. There is a need for unstinted support for the textile engineering industry from the Government as well as the textile industry. While the Government should give a strong financial support for infrastructure and R&D, the textile industry should stop importing used machinery and encourage the domestic manufacturers. The textile industry should not forget that the machinery industry was set up initially by them and they are duty bound to protect it.